A recent interview with a Charles Schwab strategist created some sensational headlines as Business Insider ran the headline, “Investors are ignoring a crucial risk that has Charles Schwab’s global strategy chief up at night — and they’ll be caught off guard as US stocks lag international equities for years

.”

A recent interview with a Charles Schwab strategist created some sensational headlines as Business Insider ran the headline, “Investors are ignoring a crucial risk that has Charles Schwab’s global strategy chief up at night — and they’ll be caught off guard as US stocks lag international equities for years

.”

In the piece, Jeffrey Kleintop, the Chief Global Investment Strategist for Charles Schwab, is described by the Insider author as having said:

Investors should hedge against the potential downsides of populism and geopolitical conflicts by owning a diverse basket of international stocks, Kleintop said.

The global strategy chief noted that non-US stocks have topped the S&P 500 since the start of this bull market in October 2022. That discrepancy would be even wider if not for the so-called Magnificent 7 growth stocks: Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla.

That outperformance streak will continue, Kleintop predicted. International equities trade at much cheaper valuations than their US peers on a forward price-to-earnings basis, even after their rally, he noted. Plus, the group will post better earnings and benefit from a falling US dollar and an improving economy, while US companies contend with positive but slowing growth.

Kleintop’s sentiments are stated in a more subdued nature in his official Schwab.com article “2024 Mid-Year Outlook: Global Stocks and Economy .”

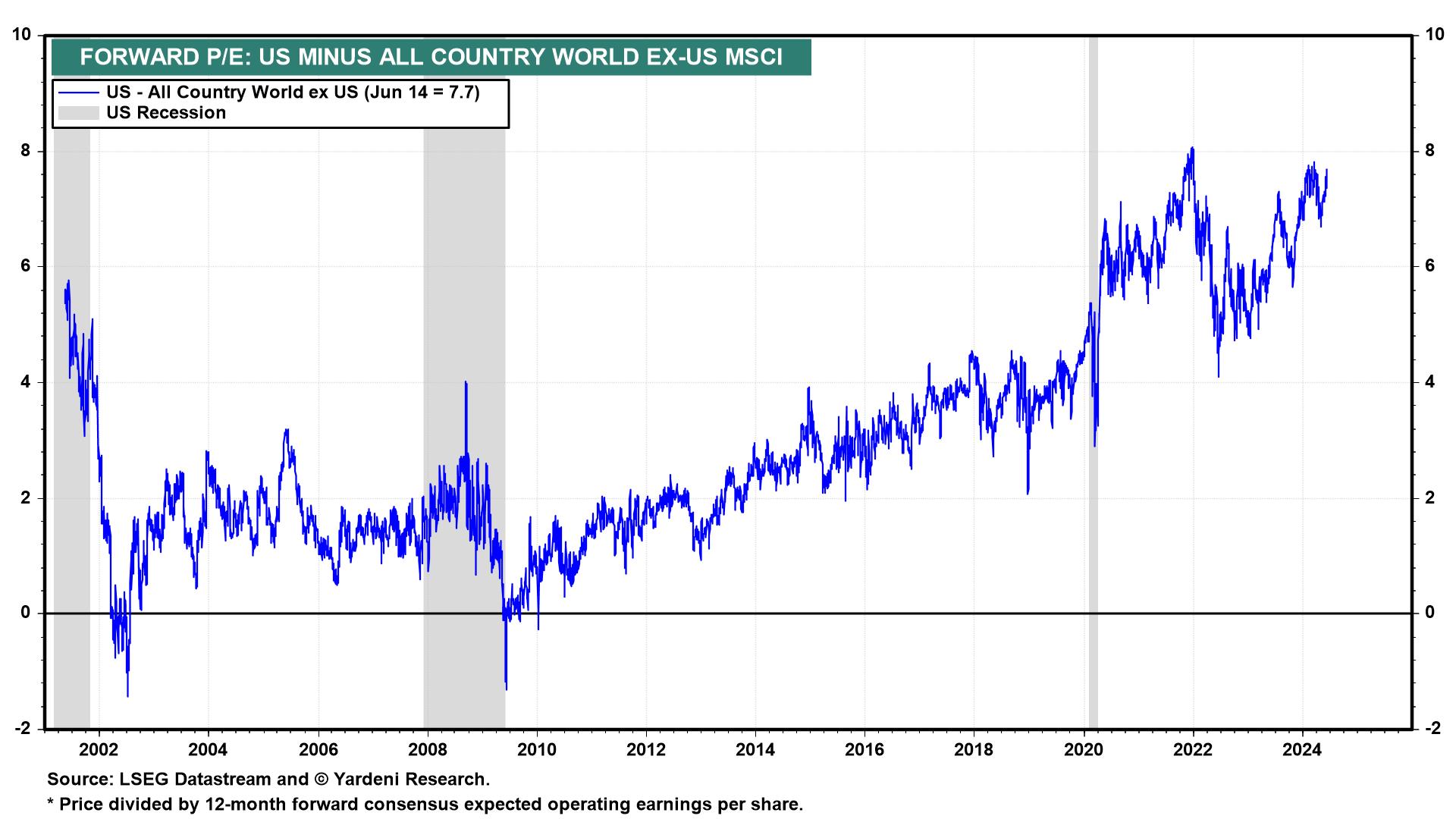

We agree with Kleintop’s assessment that valuations suggest that international equities are poised for more gains. The Yardeni Research provides “Global Index Briefing: MSCI Forward P/Es ” which shows country-specific forward price/earnings (P/Es) over time.

The below Yardeni graph (Figure 12) shows the expensiveness of the United States through a graph of the forward P/E of the United States minus the forward P/E of the all world without the United States.

You can also see from this graph that the apparent overvaluation of U.S. stocks is not a new matter, although recent valuations are outliers.

In this way, the Bloomberg headline is far too sensational for reality. It is entirely possible that the U.S. could continue to outperform global equities without a correction for longer.

However, these valuations would suggest that at some point either U.S. earnings will increase to bring the U.S. into fair valuations at the current price or the price will fall to meet current earnings where they are.

Near the end, Kleintop mentions that it is the official stance of Charles Schwab that an invasion of Taiwan “over the intermediate term” is a “low probability.” His reasoning appears to be his assumption that China’s fear of sanctions keeps them from invading. However, you can read his own words here:

In Asia, Beijing has long described reunification with Taiwan as a goal. However, China has been restrained from using military force, which would likely result in the developed world responding with negative economic consequences. With China being more significantly integrated within the global economy compared to Russia, the threat of sanctions from the rest of the world could likely cause significant damage to China’s economy. There is also a lack of popular support within Taiwan to declare independence from the mainland, preferring to maintain the status quo according to surveys conducted by National Chengchi University. We maintain our long-held view that an invasion of Taiwan by China is a low probability over the intermediate term.

It is still our opinion that if we wait to hedge against the possibility of a China-Taiwan conflict the market will have already priced in more of its fears. You can read more about our strategy for mitigating this possible risk in our articles on the topic.

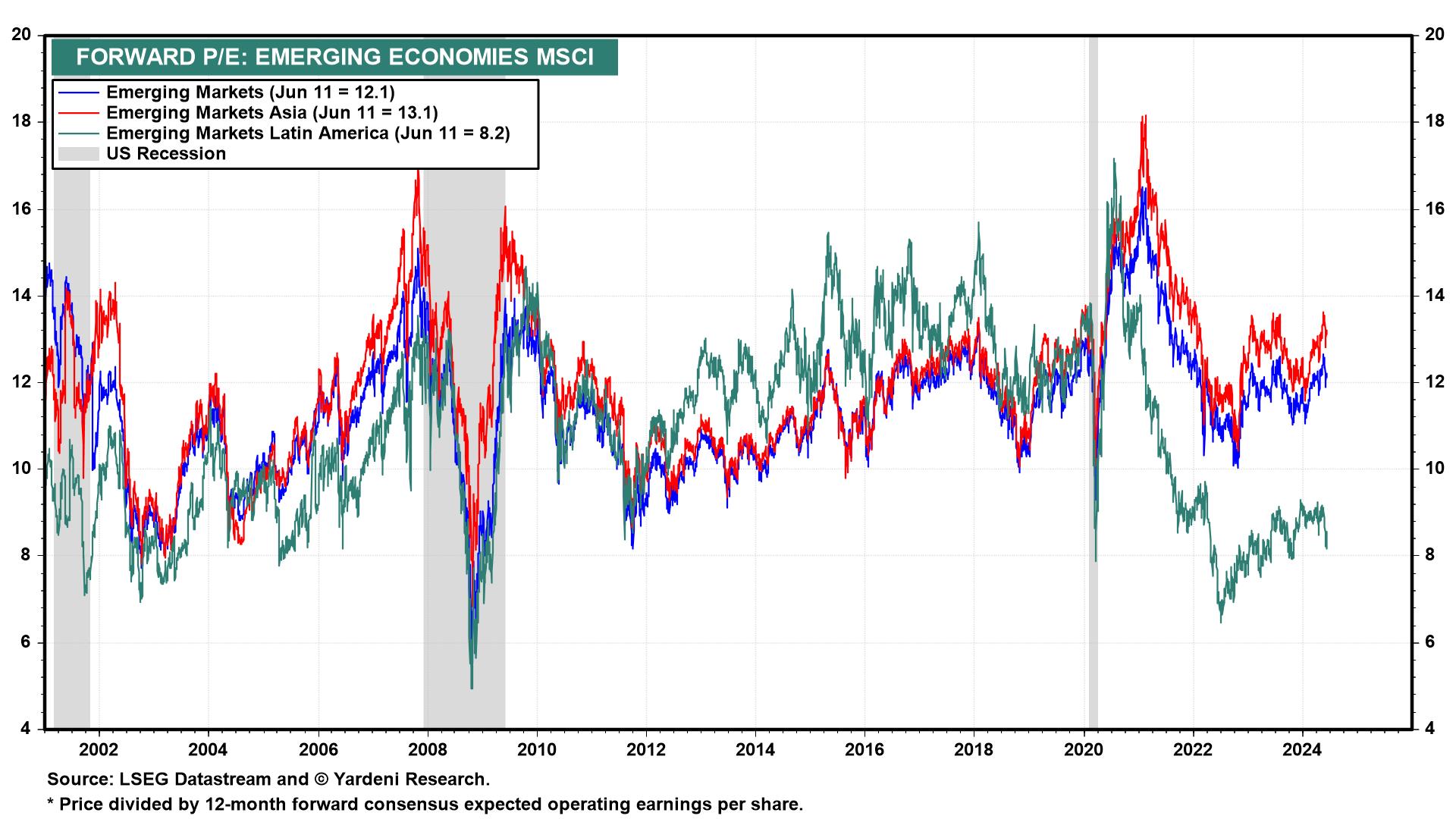

Regardless of what happens with Taiwan, Latin America Emerging Market countries like Brazil, Mexico, and Chile appear undervalued compared to Asian Emerging Market countries like Taiwan and South Korea. This can be seen in the graph below from Yardini. The green line of Latin America can be seen as cheaper than the red line of Asia.

We have no crystal ball over here at Marotta. We strive to utilize a portfolio strategy that does not require market timing to be successful. We think the contrarian effect of rebalancing on a historically justifiable portfolio gives the best chance of weathering the market ups and downs.

No one knows what the future holds. We have had a healthy foreign stock allocation all along, and we will continue to have one now.

Photo of Mexico by Jezael Melgoza on Unsplash. Image has been cropped.

Latest posts from Megan Russell

- #TBT Do I Need to Pay Tax on This 1099-R? - March 5, 2026

- Account Funding Priorities: A Savings Waterfall for 2026 - March 3, 2026

- #TBT How to Report a Backdoor Roth or Nondeductible Contribution on Your Tax Return - February 26, 2026