All new employees have to fill out form W-4. You may remember it from the heap of HR paperwork on your first day of work, but despite its ubiquity, most people don’t understand it.

How the W-4 Works

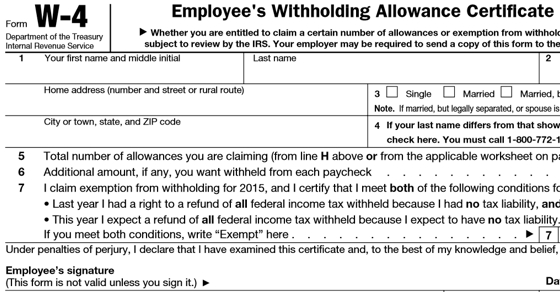

The top part of the form helps you calculate the number of “personal allowances” you can claim. Each of these equates to a $4,000 deduction from your taxable income when your employer calculates how much to withhold from each paycheck.

You’re allowed 1 allowance just for existing (unless you’re a dependent), 1 for working at the job you’re filling out the W-4 for, 1 for your spouse (if you have one), 1 for each dependent you have, 1 if you’re filing head of household, 1 if you’re taking the Child and Dependent Care Expenses Credit for at least $2,000 of expenses, and either 1 or 2 bonus allowances (depending on your income) for each child eligible for the Child Tax Credit.

For married couples, you should note that you and your spouse are required to split your allowances between the two of you. Helpfully, that information isn’t on the W-4, but it is in Publication 505.

The bottom part of the form is mostly demographic information. The only tricky spot is Line 7, which asks if you are exempt from tax withholding entirely. This is true if you owed no tax at all last year and won’t this year. Note that you can have received a tax refund but still have owed tax, so you should check the latest tax return you filed. If you are exempt, you write “Exempt” in line 7 and can skip the top part of the form entirely.

There are also two supplementary worksheets if you’re itemizing deductions and if you work two jobs or more (also, if you’re married, if you and your spouse combined have two or more jobs). If you’re itemizing, you get an extra allowance for every $4,000 your estimated deductions exceed your standard deduction and your non-wage income.

The Game is Rigged

The form is designed to withhold too much from your paycheck, which just gives the government an interest-free loan of your money. Let’s figure out how that happens.

This is how your employer has to calculate your withholding: they take your annual salary, then subtract $4,000 times the number of allowances you claimed. They figure the tax owed on that amount of money, then divide that tax owed by the number of pay periods in the year. That result is how much to withhold from each paycheck. (see Publication 15)

The problems here are numerous. The W-4 calculation doesn’t take into account any income besides your salary, and most people have some. There are some deductions and credits it just doesn’t allow to be converted into allowances, which artificially inflates the estimate of your taxable income your employer has to use. Nobody earns deductions and credits in discrete $4,000 chunks, but you can’t have fractional allowances and they don’t round up: the first $3,999 of deductions you have above the standard deduction are willfully ignored for withholding purposes and $7,999 of deductions are treated just like $4,000. Withholding isn’t figured on the amount of pay periods left in the year, but how many there are in any year regardless of the month. This means if you file a new W-4 that reduces your withholding in July, the fact that you over-withheld for half a year is ignored.

And if you never turn in a W-4, your employer counts you as Single with zero allowances. It’s actually impossible to have zero allowances – you get one for working at the company to which you didn’t submit a W-4 and unless you’re a dependent, you get another one.

Is this a stupid system? You bet. All this rigmarole obscures how the system actually works, which just makes people worry. Most people don’t know how much they are withholding or even how much they should be withholding.

All the law requires is that you withhold the amount of tax you owed last year (before withholding and credits were taken into account). You always know how much you should withhold this year by April 15th when you figure out how much you owe for the income you earned last year.

A sensible system would let you just give that number to your employer, let them divide it by the number of pay periods in the year, and withhold that. This would get your withholding exactly right, guaranteed. Instead, we have to go through an obscure process that few people understand, wasting the time of the confused employees trying to fill out the form, the employers performing unnecessary and inaccurate recalculations, and the IRS trying to explain the process to us all.

Why You Still Have To Play

Many people, aware of the fact that the form is unnecessarily confusing and rigged against employees, throw their hands up and say, “write whatever you want to get the withholding right.” They figure the IRS cares more about getting the right answer than the process used to get there. That is, of course, wrong.

There is a $500 penalty for claiming too many allowances (reducing the tax withheld from your paycheck) with no reasonable basis at the time you filed the W-4. There can also be criminal charges (up to $1,000 and a year in prison) if you willfully fill it out just to reduce your withholding.

Most people never update the form. From the rules above, it seems like you could leave an inaccurate W-4 on file forever and nobody would care. That would be true, except that whenever your number of allowances changes (like if you have a child, get married, or your itemized deductions change), you’re obligated to file a new W-4 within 10 days. And the criminal charges also apply if you willfully fail to amend your W-4.

The people telling you to make things up and not worry never read the fine print above the signature line: “Under penalties of perjury, I declare that I have examined this certificate and, to the best of my knowledge and belief, it is true, correct, and complete.”

Why You Shouldn’t Worry Too Much

The IRS has bigger fish to fry than folks who don’t withhold enough money on their W-4’s and are not otherwise engaged in shady tax dealings. As long as you actually do withhold enough money, you’re unlikely to hear anything from the IRS if your W-4 is just a little off.

And if you’re still worried about under-withholding (despite the IRS rigging the game to make that nearly impossible), they waive any penalties for under-withholding by up to $1,000.

Finally, the IRS says they won’t penalize people for making honest mistakes on the W-4, promising to only go after willful cheats.

But Isn’t it Still Stupid?

Yes, it is. But there’s no way around it – the IRS has legislated no way out from this system despite the ease with which everybody could know for sure that they’re withholding the exact right amount of tax. This is classic tax law – needless complication with meaningless variables in a calculation rigged against the well-being of the citizens but entirely opaque to them.

It’s hard to put things more strongly than this: there is absolutely no good reason for the tax withholding system to work this way.

Tips for Students

For those who are filling out paperwork for their first job and have no prior experience with the W-4, welcome to the labor force!

If you didn’t owe any tax last year and don’t this year, for example, a student at an unpaid internship, just be sure to remember your Social Security Number. You’ll enter that and basic demographic information, fill out “Exempt” on Line 7, and be done.

If you did or will owe tax, fill out the top part of the form for your personal allowances. If you’re a student, you should know whether your parents are claiming you as a dependent on their tax return this year (they probably are). If they aren’t, you can claim yourself on Line A. Then, dependent or not, enter “1” on Line B for having this job you just got. And that’s all, unless you have children yourself.

Screen capture from 2015 Form W-4.