Qualified HSA Funding Distribution

on June 19, 2016 with No Comments

There is an obscure tax rule that allows a one-time Traditional IRA-to-HSA conversion called a Qualified HSA Funding Distribution (QHFD).

David John Marotta and Megan Russell co-author a syndicated financial column featured in several newspapers across the country.

There is an obscure tax rule that allows a one-time Traditional IRA-to-HSA conversion called a Qualified HSA Funding Distribution (QHFD).

REITs are one way to get some of the benefit of investing in real estate without as much of the risk.

Life planning begins as thoughts and ultimately shapes our entire destiny.

This style of Power of Attorney certainly gets the job done, but there are a few ways that the cookie-cutter POA most frequently fails to meet people’s wishes.

Most investors think that whenever you buy or sell a security the money is immediately deducted or deposited into your account. This is not true.

Here are the four criteria which must be met in order for margin loan interest to be tax deductible.

Too much leverage is risky because it endangers meeting your goals.

We don’t normally recommend being on margin, but we recommend having the option in case it is needed.

Any legislation which can include FINRA’s commission-based advisors will dilute what it means to be a fiduciary.

Wash sale rules need to be followed when realizing capital losses for taxes but can be burdensome to track and monitor.

Even the most brilliantly crafted investment plan has to be given time to work.

This Schwab checking account provides six impressive services not true for most local banks.

Index investing seeks to track the return of a portion of the market. The opposite is active management.

An HSA is one of many accounts used in comprehensive wealth management for tax optimization and planning.

The Internal Revenue Service (IRS) is notorious for misunderstanding the recharacterizations of Roth conversions.

The University of Virginia plan includes funds sufficient to produce these excellent portfolios.

QCDs allow individuals age 70 1/2 or older to give directly to a charity from your IRA without counting the distribution as taxable income.

Here is a review of Marotta’s 2015 Vanguard Gone-Fishing Portfolio and a description of our changes for 2016.

The gone-fishing portfolio provides suggested asset allocations for investors up to age 70 and up to $1 million.

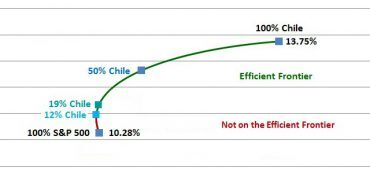

Adding a little bit of Chile to your portfolio can boost returns and reduce volatility.

These are just some examples of the creative beneficiary designations, but the important part is to dream big about what your wishes are.

We’ve written about how to select securities but in this article we are going to apply those principles to the process of selecting a specific fund for a specific sector of the economy.

Here is a simple way to think about commercial property.

For children with lower incomes, there is an opportunity to give them appreciated stock to shift the capital gains to a lower tax bracket.

The kiddie tax was first added to the tax code in 1986 for children under age 14. Now, it can burden them until they are 23.

Financial Christmas gifts don’t need to be a piggy bank. They can be more serious and more meaningful than that.

Will substitutes sacrifice some of the customization of trusts but avoid the accounting complexities.

After you reach the age of 70 1/2, the IRS requires you to begin taking minimum distributions from your traditional retirement accounts.

Assumptions about these adjustments to your net worth should be made carefully and conservatively.

Carefully computing and adding your Social Security early retirement safe withdrawal rate can safely boost your early retirement standard of living without jeopardizing your future finances.

We highly recommend a Donor Advised Fund for generous investors.

The shortest answer is yes, you can. But just because you can, doesn’t mean you should.

Regardless of the reason, if you have put too much money in your Roth IRA, the solution is the same.

Even over the income threshold, you may still be able to add funds to your Roth IRA with what is called a backdoor Roth.

You’ve opened your HSA and funded it for several years. When should you stop funding it?

If you prefer to keep your down payment money invested in the markets for longer, there are two alternatives.

Here are some rules for handling your digital security.

Which account you should fund depends on your circumstances, but here are some general guidelines you can follow to make your decision.

Umbrella insurance covers you for liability that goes above and beyond your auto and homeowners insurance.

Virginia taxpayers can give generously and offset the cost of those gifts through tax credits and the avoidance of capital gains taxes.

Most tax professionals don’t think of such tax planning opportunities, because they have to focus on complying with tax accounting regulations.

Sometimes, there isn’t enough to do it all. Even then, fund your Roth.

The average married couple has dreams of multiple children, annual vacations, and homeownership, but planning for these expenses can be challenging.

You might think that you can’t qualify, but many well-paid families are eligible.

For those who do not want to be investors, a fast-track repayment may be best. But for those willing to save and invest, there is a better option.

Careful tax planning can avoid much of the capital gains tax.

After automating your entire investment plan, you can save and invest without even having to watch.

Your investment strategy is critically important but the implementation requires wise fund selection.

As with many financial decisions, our gut feelings deceive us on this matter.

The process of defining your sectors is an attempt to identify the quintessential features of your strategy and formalize your selection criteria.