How to Be a Good Executor

on April 10, 2015

with No Comments

You’ve been named the executor of a relative’s will – now what?

You’ve been named the executor of a relative’s will – now what?

You probably have dozens of online accounts and possibly hundreds of dollars of digital property. What happens to it when you die?

What happens to my Facebook, Twitter, Wordpress, and other online accounts when I die? Could I decide?

Who do I choose to be the executor of my estate? What will their basic duties be?

Today’s question: What do I want to happen to my physical belongings and assets after my death?

Today’s question: What if something happens to me and I am not able to make decisions for myself?

It is often said that the only two certainties in life are death and taxes. The IRS takes that truism to heart.

What is a better starting place than advertisements and phone directories?

There is a tax benefit to leaving some assets to your favorite charity rather than leaving it to your heirs.

Leaving a legacy can be a great benefit for the charity receiving the gift.

When you die, your assets and belongings–called your “estate”–are subject to taxation, but the there is an amount under which the executor of your estate will not have to pay taxes.

There is a limit, or exclusion–an amount that the government will allow you to gift to a person per year, without incurring tax consequences.

It is a common assumption that your last will and testament determines who gets your stuff when you die. What you may not know is the vast majority of your assets may be transferred to others regardless of the instructions in your will.

A good estate plan is every bit as useful during your lifetime as it is at your death. No matter your age or how much (or how little) money you have, there are three essential estate planning documents you should have.

The most important product of estate planning is achieving family harmony.

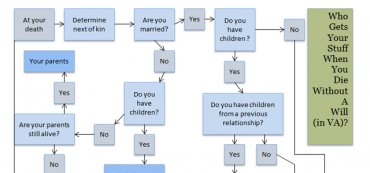

It can be tricky to figure out who your “next of kin” is, so here’s a handy flowchart to help you figure out who gets everything you leave behind if you don’t have a will.

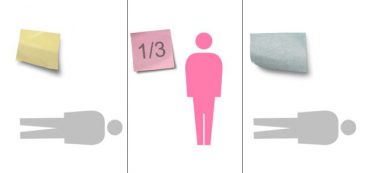

Before a grandmother passes away, both her sons predecease her. Left with only her daughter and grandchildren, depending on her titling one of three things may happen.

“They don’t deserve it!” is the most common complaint. And in most cases it’s true

The new unified credit changes for estate planning in 2013 have once again changed when you should have provisions for a bypass trust.

You should have no problem naming your nephew as your beneficiary, but accessing the money from India after your death is more complicated.

Knowing which assets to give away to your beneficiaries can save your estate and your beneficiaries big tax bills, even if you have a small net worth. If you plan on making a gift to charity from your estate, you can be even more tax savvy with your giving.

One of the most common estate planning mistakes is a plan that is implemented incorrectly. Your estate plan is only worth the paper it is printed on unless you follow through on titling your assets correctly and updating your beneficiary designations.

If you own real estate in different states, you may be leaving a mess of nightmarish proportions for your executor (the person who oversees and distributes your assets when you die). Here’s how to reduce the headache.

It may surprise you that proceeds from retirement accounts and insurance policies are not divided according to the terms in your will. Instead, these assets pass directly to the beneficiaries you named on the account.

No matter your age, in addition to a will, you need two additional documents.

The worst thing you can do is to do nothing at all and assume everything will pan out in the end. No matter how much (or how little) money you have, you need at least a simple will.

Five Wishes is a national advance directive created by the non-profit organization Aging with Dignity. It has been described as the “living will with a heart and soul.”

A thoughtful estate plan can make your heirs’ lives easier. But it is your parents’ estate planning that will make your life easier.

Your estate plan can make your heirs’ lives easier. But it is your parents’ estate planning that will make your life easier.

Bequeathing a Roth is much the same as setting up a lifetime tax-free stream of income for your heirs.

Communicating honestly about your finances with your family and putting your estate in order passes on a legacy of foresight and financial wisdom that will help generations to come.

Communicating honestly about your finances with your family and putting your estate in order passes on a legacy of foresight and financial wisdom that will help generations to come.

Estate planning must begin with family harmony as the goal. Thus personal dynamics are more important than avoiding probate and estate taxes.

The most important product of estate planning is achieving family harmony. Think carefully when you choose your executor or trustee.

How you “title” the property you own is a lot more important than you might think. Failure to title your assets properly could undo the best will and trust planning that money can buy.

A $360,000 investment can remove over $2 million from their taxable estate, savings $900,706 in estate taxes.

Unlike the trusts which helped John D. Rockefeller and J.P. Morgan keep their wealth in the family, this new breed of dynasty trust is not just for the mega-wealthy.

Only 34% of family businesses successfully pass to the second generation and only 13% make it to the third generation.

Many financial products are sold through greed or fear, but estate planning isn’t one of them. Having an estate plan and a living trust is an import part of wealth management.

If you think estate planning information is hard for you to pull together, imagine how difficult it will be for someone else who is asked to fill your shoes in an emergency!