In my 2019 article “Do Dividend Paying Stocks Make Better Investments?” I wrote:

In my 2019 article “Do Dividend Paying Stocks Make Better Investments?” I wrote:

Investors mistakenly believe that dividend paying stocks make better investments. A company paying dividends is thought to have a more concrete valuation and the dividends are beloved by retirees who can visually see the dividends supporting their withdrawals. In other words, dividends are loved because you can take your dividends to the bank and spend them.

In reality, maximizing dividends merely serves to minimize appreciation. While appreciation is taxable only when gains are realized, dividends are taxable each year. This means that dividend paying stocks may amplify The Costly Effect Of Saving In A Taxable Account.

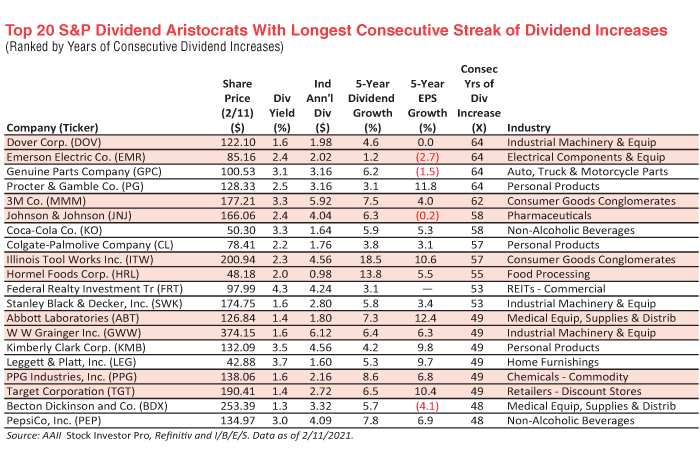

Five years ago, a March 2021 AAII article entitled “Dividend Aristocrats With Longest Streak of Dividend Increases” highlighted a group of such companies, and I saved the article anticipating that these 20 stocks would not out perform the value stock index they came from.

Now that it has been five years, we can return to that article and do the analysis of how the dividend aristocrats performed compared with value stocks generally. Here is the table from the 2021 article:

For this analysis, I used total returns from March 1, 2021 through March 1, 2026.

Of these twenty individual stocks, the one with the highest return was GWW, up +211.18%. The one with the lowest return was LEG, down -67.43%. The volatility between these two is part of the dangers of individual stock investing.

As a whole, the twenty stocks were up +34.51% over the five years or 6.11% annually. Had you failed to include GWW, you would have only received a return of 25.21% or 4.60% annually, under performing by -9.30% or -1.51% annually. Often missing out on the best stock significantly hurts returns.

Individual stock selection increases your standard deviation and therefore the risk of not meeting your financial goals. A wider scatter plot of potential returns causes some of those potential returns to fall below the minimum return necessary to meet your goals. It requires a large number of individual stocks before individual stock risk is diversified out of a portfolio.

This is why we favor exchange traded funds such as Vanguard Value (VTV) with over 300 individual stocks. It not only provides a smoother return than individual stocks but it can also provide superior returns.

VTV was up +84.56% over the same five year period or 13.04% annually. Investing in VTV rather than these twenty stocks produced 50% more money, lower volatility, and less complexity.

Valuation can be more significant for future return than dividend yield. Dividend investing asks, “Which companies are paying out cash?” Value investing asks, “Which companies are priced cheaply relative to fundamentals?” Those are not the same question.

Dividends are also a less tax-efficient way to compound wealth. Even when dividends are qualified and taxed at a lower tax rate, they are still taxed, and that tax payment cannot be reinvested to receive compounding.

Dividend aristocrats may be admirable companies, but admirable companies are not always the best investments. For long-term portfolio design, valuation matters more than yield, and broad value exposure is often better than a narrow preference for dividend payers.

Photo by Geoffrey Noake on Unsplash. Image has been cropped.